Well before the media anointed mobile the Next Big Thing, venture capitalists saw its potential. Consumers have rewarded VCs for their foresight by how quickly they’ve adopted non-voice mobile services over these past couple of years. The result has been a number of high-profile liquidity events this year starting with mobile ad network Millennial Media’s IPO followed by Facebook’s acquisition of Instagram for an eventual price of $736 million and record levels of gaming sector acquisitions led by mobile. With all this positive momentum it’s not surprising that VCs continue to allocate an increasing share of deals and dollars to mobile startups as the overall number of investments has reached its highest levels since the dot-com days.

Well before the media anointed mobile the Next Big Thing, venture capitalists saw its potential. Consumers have rewarded VCs for their foresight by how quickly they’ve adopted non-voice mobile services over these past couple of years. The result has been a number of high-profile liquidity events this year starting with mobile ad network Millennial Media’s IPO followed by Facebook’s acquisition of Instagram for an eventual price of $736 million and record levels of gaming sector acquisitions led by mobile. With all this positive momentum it’s not surprising that VCs continue to allocate an increasing share of deals and dollars to mobile startups as the overall number of investments has reached its highest levels since the dot-com days.

In contrast to this optimism in the venture community, Wall Street is down right negative towards mobile. Google’s third quarter earnings announcement was met with a 8% drop in share price in part due to the increasing number of search queries being performed on mobile devices which is causing a deceleration in the company’s revenue growth. And while Facebook’s most recent quarterly earnings report resulted in the stock rising 20%, the company’s market capitalization is still only at 60% of its peak value from its first day of trading. This is in largely due to concerns over Facebook’s ability to monetize their growing mobile audience, which now consists of 600 million users, including 126 million of which use Facebook mobile exclusively.

The Typical Relationship

So why the disconnect in how these investors value mobile? It can be partially explained by how each type of investor evaluates investment opportunities to begin with. Venture capitalists, especially early stage ones, typically look to buy private, and thus illiquid, stock in pre-revenue companies with nascent, but potentially market-disruptive, ideas. As such, these investments may take up to 10 years to realize a return for their VCs, if at all. Contrast this with public market investors, such as hedge and mutual funds, which focus on the predictability of earnings and revenue growth relative to a company’s market value and reevaluate their investments in real-time based on news and quarterly earnings reports since liquidity is readily available in these stocks.

So when VCs invest in start-ups, especially consumer-oriented ones that are ad-supported, they are betting not only on a company’s potential to execute on their business plan but also on the formation of a rapidly growing market. Due to this, the focus is usually on customer acquisition and market share growth- not revenues. As a market begins to mature in size and opportunity, monetization solutions are developed, usually by other start-ups, allowing the entire market to benefit from the creation of new revenue streams. Companies that don’t get acquired and can show they have a path to profitability have the opportunity to go public and in the process become industry bellwethers, using their new capital infusion and stock shares as currency to further enhance their market position.

Why Mobile Had Been Different

In the case of mobile, a couple of things happened that has affected the usual relationship between the private and public markets. First, the consumer adoption of mobile has outpaced any other technology in the history of the U.S.- including radio, TV and the internet. As such the native monetization solutions that were developed alongside these other technologies have been slow to scale in mobile because (1) the ad formats currently being used are largely re-purposed ad technologies from the desktop internet, such as banner and rich media ads, which were easy to launch with in an effort to capture mobile revenue early on and (2) advertisers have been slower to allocate advertising budgets to mobile than previous technologies due to this speed of growth- funds that would be used to help spur innovation in ad experiences on mobile devices.

The economic realities of increasing supply of mobile ad inventory coupled with relatively low demand for quality ad experiences thus far has resulted in effective CPMs that are 1/5th the price of desktop internet advertising. This disparity in monetization capabilities between mobile and desktop is forcing public investors to reevaluate consumer tech investments where mobile is becoming impactful enough from a usage perspective to potentially affecting earnings. With Millennial Media, a pure-play mobile ad network, and Pandora Media, whose ad-supported internet radio audience is now 75% mobile, still not profitable as publicly-traded companies, investors will continue to discount the mobile businesses of public consumer technology companies for the foreseeable future.

Without having proven their business models to Wall Street yet, Millennial and Pandora can’t be considered mobile bellwethers, which is needed to preserve the private-to-public valuation relationship. Companies such as AdMob and Instagram might have achieved bellwether status if they hadn’t been acquired before realizing their potential as stand-alone public companies. As such it might be left to existing ad-supported consumer internet tech leaders who are able to make the audience and business transition into mobile to perpetuate the ecosystem. Facebook, which has faced scrutiny over its performance as a public company in part due to mobile, has the momentum in user growth and sheer audience size to accomplish this transformation if they can prove their various mobile ad products can profitably scale. Because of this you could argue that Facebook actually went public too early, instead of too late, if you look at it as a mobile-first company. Probably the best positioned public company though is Google which acquired what is now the most popular mobile operating system in Android, largest mobile ad network in AdMob and is seeing mobile growth in its core search business as well as across YouTube.

Mobile is Really Two Different Experiences

The second part of the answer to the valuation disconnect is in the definition of mobile. When research companies forecast trends and investors talk about opportunities they always speak about mobile as if it were one cohesive distribution channel when in fact it is composed of two distinct experiences- smartphones and tablets. Being able to differentiate between the two is critical because of the activities each device is best suited for based on the physical limitations of each display as well as their monetization opportunities.

Smartphones

While Apple might be credited with ushering in the consumer mobile era with the launch of the iPhone in 2007, it was the launch of the App Store the following year that enabled smartphones to properly leverage their mobility as the physical limitations of mobile phone screens (3 to 5 inches in length) required task-specific applications be built instead of all-encompassing web experiences. Because of this, the most successful app experiences, as Benchmark Capital’s Matt Cohler eloquently describes it, mimic a remote control in that they are easy to use and provide a specific utility to consumers. In turn, advertising on mobile phones need to abide by these same principles in order to be valuable.

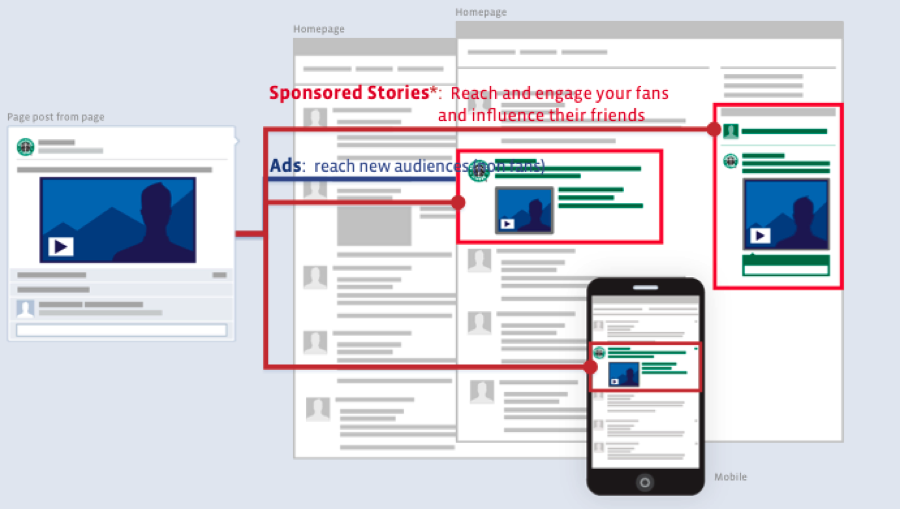

Rare Crowd’s Eric Picard described the current mobile ad format problem in a recent article while also presenting a possible solution for smartphones that is interruptive without being intrusive- and can be delivered at scale. For app developers that have large enough user-bases though, creating native experiences, especially ones that can leverage location, will always result in better value for both the advertiser and consumer. Expanding on sponsored ad units that Facebook (via Sponsored Stories) and Twitter (via Promoted Tweets) have popularized in the social activity stream and more recently on mobile, location-based social exploration platform Foursquare launched Promoted Updates for local merchants this past summer and crowd-sourced traffic app Waze launched its own self-service advertising platform earlier this month that focuses on solving users’ location-based needs.

Tablets

Like smartphones, Apple can also be credited with jump-starting the tablet market a mere 3 years ago. The company was prescient in introducing the iPad as a tool for consuming media as users have made watching TV shows, playing games and reading the primary uses for the device. This makes sense when you consider the screen size of tablets (ranging from 7 to 10 inches) allows consumers to replicate the offline experience of reading a magazine or watching television in a more convenient and personal format than traditional computers allow for. Because of this, advertising on mobile tablets can be interruptive like traditional media and less concerned with other vectors such as location since most people are using their tablets at home and as a second screen complement to watching television. That means online video and rich media interstitials, which are higher-valued ad units than traditional banner ads, will work with minimal refactoring compared to smartphone ad experiences. That doesn’t mean there isn’t an opportunity for companies to innovate around the ad experience as start-ups like Kiip are proving by rewarding user engagement and retention within mobile apps with real world rewards.

When It’s All Said and Done

With tablets expected to outsell PCs by next year, focusing efforts on this part of the mobile market might be the most prudent move for consumer tech companies with mobile audiences since the advertising experience most closely resembles the desktop internet from both a format and value perspective. The smartphone advertising market will take longer to scale simply because of the utility-oriented nature of the user experience.

As these advertising solutions sort themselves out though, so should the discrepancy between public and private market investor valuations around ad-supported business models. As start-ups fill these gaps in the consumer mobile space with monetization solutions that prove to be effective, so to will public investors get comfortable with the long-term value mobile users have to offer, which, at the end of the day, will benefit everyone involved in growing the value of the mobile industry.